Business valuations divorce refers to valuing business interests so the Federal Circuit and Family Court of Australia can divide property fairly under the Family Law Act 1975 (Cth). A single expert valuer is commonly appointed, using methods like capitalisation of earnings or discounted cash flow. Outcomes include buyouts, sales, or staged payments, with tax and cash flow carefully managed.

Key Legal Points

- Business valuations divorce values business interests for Australian family law settlements

- The Court uses a four-step approach assessing asset pool, contributions, and needs

- Single expert valuers and clear instructions produce reliable market-aligned opinions

- Time limits apply, usually 12 months after divorce or two years de facto

- Costs vary widely; scope and documentation quality significantly influence fees

- Buyouts, sales, or deferred structures can equalise entitlements while preserving cash flow

- Normalising earnings, owner’s remuneration, and working capital are critical adjustments

Business valuations divorce refers to the process of determining the fair market value of a business interest so it can be considered in a family law property settlement. Asset division then allocates that value, along with other assets and liabilities, between separating spouses under Australian family law.

Business Valuations Divorce: Legal Framework and Definitions

Legal Framework

Under the Family Law Act 1975 (Cth), the Federal Circuit and Family Court of Australia determines just and equitable property settlements. The Court applies a four-step approach that incorporates business valuations divorce to assess the asset pool, contributions, future needs, and whether the proposed orders are fair. Company structures are also relevant under the Corporations Act 2001 (Cth).

For the statutory basis of altering property interests for married couples, see Family Law Act 1975 (Cth) section 79. For de facto couples, section 90SM is applied. The same valuation principles usually apply across both categories.

Key Definitions

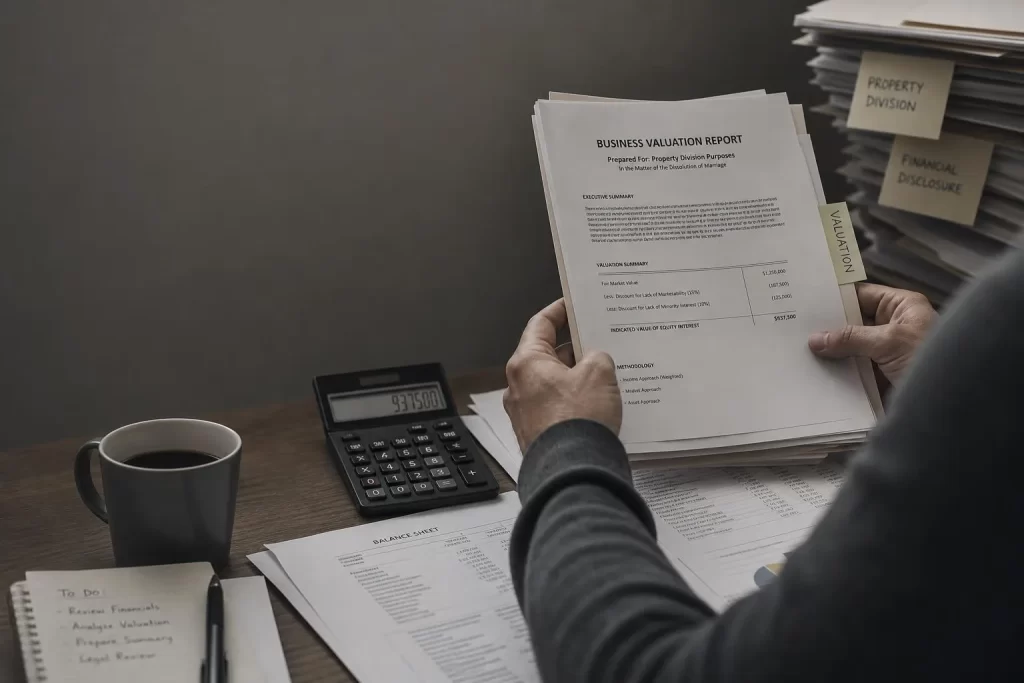

Business valuations divorce means valuing a sole trader, partnership, company, or trust interest at a specific date. The Court prefers an independent single expert, unless a different approach is justified.

- Asset pool means all assets, liabilities, superannuation, and financial resources

- Fair market value means the price between a willing but not anxious buyer and seller

- Single expert means a jointly engaged valuer whose report can be tested but is prima facie evidence

Common Search Intents We Address

- How to value a business in a divorce

- How dividing business in divorce works with different structures

- Whether one spouse can keep the business and how to equalise

- How to manage tax, cash flow, and timing risks

- What evidence the Court expects for business asset division

Process and Steps for Business Asset Division

Step-by-step Valuation and Settlement Process

- Identify the business interests, related entities, and trusts

- Collect financial records, including management accounts and tax returns

- Agree instructions and appoint a single expert valuer

- Finalise the valuation methodology and valuation date

- Consider adjustments for non-commercial loans, cash drawings, and shareholder funds

- Negotiate division options, e.g. buyout, sale, or deferred payments

- Formalise by consent orders or a binding financial agreement

In real scenarios, we see disagreements about the valuation date, normalisation adjustments, and owner’s remuneration. Early clarity on these items reduces cost and delay.

Documentation Needed

- Constitution, shareholders’ agreements, unit or trust deeds, partnership agreements

- Three to five years of financial statements and tax returns

- Management accounts, budgets, and forecasts

- Key contracts, leases, IP, loan agreements, related party transactions

- Customer concentration and staff retention data

How Business Structures Affect Division

Dividing business in divorce differs for sole traders, partnerships, companies, and trusts. Control, transfer restrictions, and retained earnings influence outcomes. Business valuation family law analysis considers commercial realities, not just book values or tax figures.

Valuation Methods and Practical Issues

Common Valuation Approaches

- Capitalisation of future maintainable earnings for stable SMEs

- Discounted cash flow for growth or project-based enterprises

- Asset-based methods for holding entities or asset-heavy businesses

Business valuations divorce often hinges on normalising earnings, market multiples, and the reasonableness of owner’s wages. Industry risk and customer churn can justify discounts.

Adjustments and Normalisations

Valuers may adjust for non-commercial expenses, personal benefits, one-off items, and underpaid or overpaid remuneration. They will also consider working capital requirements and contingent liabilities.

Timing, Market Conditions, and Covid-era Effects

Market volatility affects value. In practice, a valuation date closer to settlement may be needed if conditions have materially changed. Business valuations divorce frequently requires updated short-form addenda when trading shifts quickly.

Options to Divide or Retain the Business

Buyout, Sale, or Co-ownership

- One spouse buys the other out, often with an equalising cash payment

- Sell the business to a third party and divide net proceeds

- Temporary co-ownership with governance rules, rarely long term

Business asset division should align with the capacity to fund buyouts without crippling cash flow. Deferred payments or earn-outs can bridge valuation gaps if carefully documented.

Tax and Cash Flow Planning

CGT, GST, and stamp duty may arise. Roll-over relief can sometimes apply. Sensible settlement structures spread payments to manage tax and liquidity. Professional tax advice should run in tandem with business valuation family law negotiations.

Protecting Operations and Staff

Keep customers and staff informed only on a need-to-know basis. Non-disparagement and restraint clauses may be required. In family law mediations, practical undertakings can preserve business value during negotiations.

Business Valuations Divorce: Common Mistakes

What to Avoid

- Using a partisan accountant instead of a single expert valuer

- Setting an unrealistic valuation date disconnected from trading conditions

- Ignoring working capital or debt when calculating a buyout sum

- Overlooking tax, director loans, and contingent liabilities

Real-world Examples

Common patterns include one party assuming the ‘book value’ equals market value, or excluding personal expenses that inflate earnings. Another frequent error is underestimating how customer loss during separation can depress maintainable earnings.

Deadlines, Limits, and Costs

Time Limits after Separation

For married couples, applications must generally be filed within 12 months of divorce. For de facto couples, the limit is generally two years after separation. Extensions are possible but not guaranteed, so start business valuations divorce promptly.

Financial Considerations

Single expert valuation fees for SMEs often range from A$5,000 to A$25,000, more for complex groups. Add costs for disclosure, legal advice, and potential tax modelling. Sensible scoping and clear instructions reduce wasted expense.

Consequences of Poor Valuation or Division

What Happens if the Value is Wrong

If the valuation is materially inaccurate, settlements can skew unfairly. Correcting errors later is costly and uncertain. Courts prefer finality, so business valuations divorce should be robust from the outset.

Compliance and Enforcement

Consent orders are enforceable. Breaches may lead to enforcement applications or costs orders. Where ongoing payments fund a buyout, default clauses, securities, and charges should be documented to protect both sides.

How to Resolve Disputes and Next Steps

Negotiation and Mediation

Early mediation with a reliable single expert can settle most matters. Learn more about practical settlement approaches in Asset Division Divorce, which complements business valuations divorce by explaining broader property pools and trade-offs.

Formalising the Deal

Use consent orders or a binding financial agreement to finalise terms. Include security for deferred sums, warranties about records, and restraint clauses where appropriate. Expert assistance with property settlement strategy is available through Property Settlements After Separation.

Practical Tips and Examples for Business Owners

Immediate Risk Controls

- Ringfence business cash, maintain ordinary wages, and freeze non-essential capex

- Document interim access, cards, vehicles, and IT to avoid misuse allegations

- Keep clean management accounts to support business valuations divorce

Examples We Commonly See

- A café owner agrees a staged buyout tied to seasonal cash flow to avoid insolvency

- A consultancy adopts an earn-out tied to client retention where goodwill hinges on one spouse

- A manufacturer sells surplus equipment first to fund a partial equalisation payment

Frequently Overlooked Technical Points

Restrictions on Transfer and Control

Shareholder agreements, pre-emption rights, and bank covenants can restrict transfers. Business valuations divorce must test whether a buyout is feasible within these constraints.

Personal Goodwill Versus Enterprise Goodwill

Where goodwill is personal to one spouse, risk-adjusted multiples may be lower. Succession planning and restraints can mitigate this, improving settlement options and value stability.

Frequently Asked Questions

Who chooses the business valuer in an Australian divorce?

The parties usually appoint a single expert valuer by agreement, with defined instructions and a common brief. If they cannot agree, the Court can appoint a single expert. Either party may ask written questions and, if necessary, seek leave to rely on a shadow expert to critique methodology.

What valuation date is used for business interests?

There is no fixed rule. The Court often prefers a valuation date close to settlement or hearing, especially if trading conditions have changed. Parties can agree a date, but material changes in performance may justify obtaining an updated addendum before finalising orders.

Can one spouse keep the business and pay the other out?

Yes, commonly through an equalising payment funded by cash, refinance, staged instalments, or an earn-out. Orders should address securities, interest, default events, and tax consequences. A carefully scoped structure reduces insolvency risk and protects ongoing trading viability.

How do taxes affect dividing a business in divorce?

CGT, GST, and sometimes stamp duty can arise depending on asset type and structure. Some roll-overs may be available. Settlement design should factor timing of disposals, available concessions, and cash flow to fund tax. Coordinated legal and tax advice is critical before signing orders.

What documents does a valuer typically require?

Three to five years of financial statements and tax returns, current management accounts, budgets and forecasts, key contracts, leases, funding documents, shareholder or trust deeds, and details of related party transactions. Clear records on owner’s remuneration and personal expenses are essential for normalisation.

Are discounts applied for small, owner-dependent businesses?

Often yes. Where goodwill depends on one spouse’s skill or relationships, valuers may apply higher risk premiums or lower multiples. Restraints, handover plans, and retention strategies can mitigate risk and may support a stronger value if implemented credibly.

Legal Disclaimer

Important Notice: The information provided on this website is for general informational purposes only and should not be considered as specific legal advice. Laws may vary between Australian states and territories, and legal requirements can change over time.

For specific legal advice regarding your individual circumstances, please consult with a qualified Australian legal practitioner who can provide guidance tailored to your particular situation.

This content is accurate as of the date of publication. We recommend seeking current legal advice for any legal matters.